We were a week late on the closing (we were hoping to close on Day 91, which was last Thursday and the earliest we were legally allowed to close), but we finally got The Unexpected House closed…

The project was easy and profitable, and other than having to wait 2 months to close (due to the deed restriction) and the appraisal coming in a little low, there were no surprises. This was another good testimonial on how lucrative short sales can be!

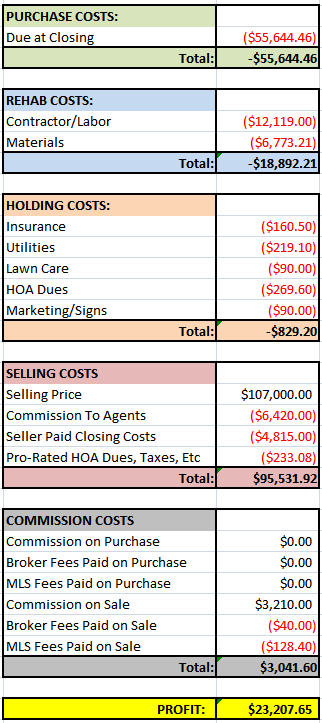

Here is the full final analysis for this one…

Timelines

Here are the key timeline milestones:

- Purchase Offer Date: 1/12/2012

- Purchase Closing Date: 2/16/2012

- Rehab Completion Date: 3/13/2012

- Sale Listing Date: 3/14/2012

- First Sale Contract Date: 3/20/2012

- Final Sale Contract Date: 3/20/2012

- Sale Closing Date: 5/25/2012

Financials

Here is the breakdown of financials for this project:

Final Statistics

Here are just some of the final statistics that I’ve been tracking for all my projects, and that summarize the success/failure of each project pretty well:

- From Offer to Purchase Time: 35 Days

- Rehab Time: 13 Days

- Selling Days on Market: 6 Days

- Selling Close Time: 66 Days

- Total Hold Time (Close to Close): 99 Days

- Total Profit: $23,207.65

- Return on Investment (ROI): 30.79%

- Annualized ROI: 113.53%

Congrats on getting another one closed! I’m curious about your seller concessions for buyer’s closing costs on this one. It’s almost $5K on a $107K house. Why so much? What did the buyer’s need on this one? Would it have been a deal breaker if you had cut it off at $3K?

Hi Kristine,

This sale was to a NACA buyer. I’m not sure how much you know about NACA, but it’s a non-profit program in partnership with a couple of the big lenders (Bank of America is the main one), where generally lower-income buyers have the ability to buy down their interest rates at the closing to keep their payments low. The most common way to buy down the interest rates is to have the sellers contribute more towards closing costs.

We do a lot of NACA deals, so we’re accustomed to paying higher-than-average closing costs for these sales. The advantage on our side is that NACA deals almost ALWAYS close, as the buyer goes through underwriting PRIOR to putting an offer on a house. So, by the time we get an offer, we know for certain the buyer is qualified. We also like NACA because their buyers actually have the lowest default rate of any major mortgage program out there — about one-half of one percent! This doesn’t impact our business, but we love supporting programs that are very pro-buyer and do a great job of keeping buyers in their houses.