After closing on the sale of The Poor House two days ago, today we closed on the sale of The Neighbor House…you can see the detailed financial results below…

This was supposed to be a quick wholesale deal to another investor (i.e., no rehab work on our part), but it ultimately took nearly two months. We found buyers for the property relatively quickly (two investors looking to try their first flip), but they had some issues with their financing. Their first loan fell apart due to some issues with the way their broker was charging fees, and their second loan dragged out for several weeks before they realized there was an issue. It turns out that they had applied for a non-owner-occupant investor loan, which is essentially a loan for a rental property. Given this was a flip project, the lender wasn’t happy about the fact that the house needed so many repairs, and the loan pretty much stalled.

Earlier this week, the investors decided to pay cash instead of trying to get the loan, and we closed this afternoon.

Had I known they were attempting to get a “rental property” loan, I would have advised them several weeks ago to go the cash route…trying to get typical investor loans for flip properties is always a long and difficult process. The worst part is that due to the long delay waiting for their financing, the buyers have pushed out starting the rehab, and have likely pushed the listing of the property out to near the end of the tax credit period (April 30), which will make it much harder to sell the property. I hope that’s not the case, but certainly come May 1, it’s going to be tougher to find buyers.

Here are more detailed breakdowns of our final schedules and financial results for this wholesale project…

Timelines

The total holding time on this house was 53 days. Had the buyers paid cash upfront instead of trying to get financing, it would have been closer to 20 days, which is what I originally had expected. It was a good lesson learned about ensuring wholesale buyers have their financing in order.

Here are the key timeline milestones:

- Purchase Offer Date: 12/19/2009

- Purchase Closing Date: 1/25/2010

- Rehab Completion Date: 1/25/2010

- Sale Listing Date: 1/26/2010

- First Sale Contract Date: 2/16/2010

- Final Sale Contract Date: 2/16/2010

- Sale Closing Date: 3/19/2010

Financials

This was a pretty standard wholesale deal in terms of profit for us, though as mentioned above, it took longer than expected to complete the deal.

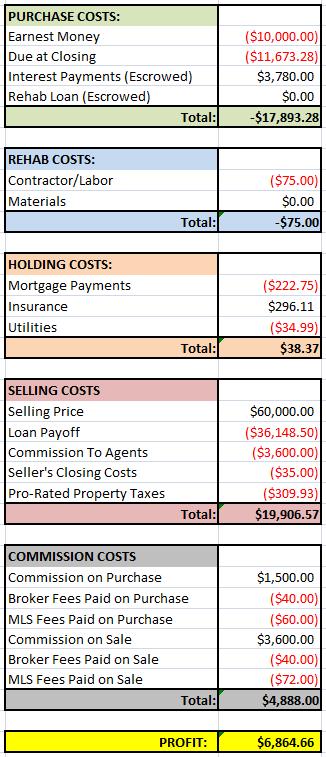

Here is the breakdown of financials for this project:

Our ROI on this project was 41% and our annualized ROI was about 286%.

Final Statistics

Here are just some of the final statistics that I’ve been tracking for all my projects, and that summarize the success/failure of each project pretty well:

- From Offer to Purchase Time: 46 Days

- Rehab Time: 0 Days

- Selling Days on Market: 21 Days

- Selling Close Time: 31 Days

- Total Hold Time (Close to Close): 53 Days

- Total Profit: $6,864.66

- Return on Investment (ROI): 41.53%

- Annualized ROI: 286.00%

Could you explain a bit about your analysis? Why are interest pmts a credit?

Also you are earning the commission on the purchase and sale? Looks like thats where the real profit was! Thanks, your blog is great.

Hey Mike –

Yup, I understand why those things could be confusing…let me explain:

– With the mortgage (interest) payments, my lender requires that I escrow one year of mortgage payments at the time of closing. In other words, at closing for this property, I paid an extra $3780 that went right into an escrow account, and my monthly mortgage payments were pulled from that account each month (i.e., the money was still mine until the mortgage payments were due each month). While this shows up as a credit under “Purchase Costs,” note that it also shows up as a debit as part of the $11,673.28 that I paid at closing. In other words, had I not had to pay this money into escrow, the $3780 credit wouldn’t be there *AND* the total amount paid at closing would have been reduced by $3780. So, you can see that this actually evens out under the “Purchase Costs” line items, as if this money wasn’t even paid.

– So, you might ask, where is the line item for the money they *did* take from me for mortgage payments? If you look under “Holding Costs,” you’ll see a line item for mortgage payments with a total of $222.75. This was one month’s mortgage interest payment that was taken directly from the escrow account before I sold the property.

– Now, if you add the $3870 that I paid at closing into escrow and the -$222.75 they took out for mortgage payments, the balance ($3647.25) was returned to me after the closing.

Does that make sense? I know it’s confusing, and to be honest, when I first tried to figure out how to account for it, it took a few minutes to wrap my head around. But, if you can imagine that money actually moving from the closing table to an escrow account, having the monthly payments deducted and then the balance coming back to me later, it should make sense.

As for the commissions, yes, my wife is a realtor and therefore got a commission on both ends. Keep in mind that the purchase commission actually came from the bank (the seller of the property when we bought it), so that was money we really earned.

But, the $3600 that shows up as the “Commission on Sale” is actually just an accounting detail. The credit you see is the commission I paid my wife on the sale, but it reduced my total income on the sale as well by the same amount (note the -$3600 paid to agents under “Selling Costs”). So, we didn’t really earn an extra $3600…it’s just accounted for as a commission profit instead of an increased sale profit. We do this for tax reasons — it’s easier for my wife to take deductions for her real estate work if she has income.

Btw, it would have been just as easy to not pay her a commission, in which case, the line item “Commission to Agents” would have been $0 and “Commission on Sale” would have been $0 as well. Same result for the net profit, but my CPA would have complained that my wife didn’t show any income as an agent.

Does that make sense?

Wow, thanks for the in-depth response. Makes sense, too.

Hi Scott,

In your analyses do you take your own salary (or the salaryof your wife into consideration) or do you take your salaries out of your profits? I can see you did consider them here http://www.123flip.com/sfh-investment-plan-part-ii/ but I can’t seem to find them on these final analyzes.

Frantz,

Salary isn’t taken out of the profits of the individual houses. Our salary/income comes from all the business profits.